Do You Skip a Mortgage Payment When You Refinance? Not Exactly

One of the most common things homeowners hear about refinancing is this:

“You get to skip a mortgage payment.”

It sounds great. Almost magical, really. Refinance the loan, take a breath, and enjoy a month without making a payment. But that idea is misleading.

Yes, your payment schedule changes during a refinance. Yes, there may be a period where you are not making your old mortgage payment or your new one yet. But no, you are not getting a free month of housing.

That “skipped payment” is not a gift. It is a timing shift. Let’s break down where this idea comes from, why it sticks around, and what is actually happening during a refinance.

Where the “skip a payment” idea comes from

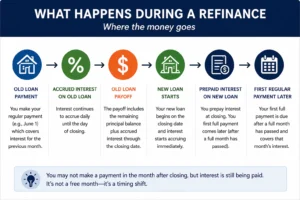

When you refinance, your old mortgage gets paid off and replaced with a new one. Because of how mortgage interest is paid and how closing dates line up, your payment schedule resets.

Here is what usually happens:

If you close on a refinance in the middle of a month, your old loan is paid off at closing. Your new loan typically will not have its first full monthly payment due until the first day of the month after next. That creates the appearance of a gap.

For example, if you close in June, your first new mortgage payment may not be due until August 1.

So people say, “Great, I skipped July.” Not quite.

What actually happens during a refinance

The missing piece is this: Mortgage interest is paid in arrears. That means your monthly mortgage payment covers the interest that accrued in the previous month, not the current one. So when you make your normal mortgage payment on June 1, you are generally paying the interest for May.

If you refinance and close on June 15, your old mortgage is paid off. But between June 1 and June 15, interest has still been accruing on that old loan. That interest does not disappear. It is collected as part of your payoff at closing.

Then your new loan begins accruing interest immediately from the day it funds. At closing, you typically prepay interest on the new loan for the remaining days of that month. This is called prepaid interest. Then, because mortgage payments are paid in arrears, your first full payment on the new loan is due after a full month has passed.

So what feels like a skipped payment is really this:

- You paid off accrued interest on the old loan at closing.

- You prepaid some interest on the new loan at closing.

- Your first regular payment on the new loan is delayed because of how mortgage billing works.No free lunch. Just different timing.

Why this matters

The phrase “skip a payment” can create the wrong expectation. Some borrowers hear it and think:

- “I get a month of no housing expense.”

- “I am saving money by not making that payment.”

- “This refinance puts cash back in my pocket immediately.”

That is where the confusion starts. In reality, you are not avoiding interest. You are not dodging a month of cost. You are simply moving when and how those costs are paid. In some cases, the timing may help with monthly cash flow. That can absolutely be useful. But it is not the same thing as eliminating a payment.

That distinction matters, especially if you are comparing refinance options and trying to understand the real cost.

A simple example:

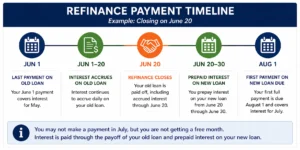

Let’s say your current mortgage payment is due on June 1. You refinance and close on June 20.

Here is what happens:

- Your June 1 payment covered May’s interest on your old mortgage.

- From June 1 through June 20, interest accrued on the old loan and gets paid off at closing.

- Your new loan starts on June 20.

- You prepay interest on the new loan from June 20 through June 30 at closing.

- Your first new mortgage payment is due August 1, which typically covers interest for July.

So yes, you may not make a payment in July. But that does not mean June and July were free. The costs were just handled differently.

Why lenders and loan officers say it

To be fair, this phrase did not come out of nowhere. From a practical, consumer-facing point of view, a borrower may go a month without writing a mortgage check. That feels like skipping a payment, and people naturally describe it that way.

But the phrase is incomplete. A better way to say it would be:

“You may have a gap before your first new mortgage payment is due, but you are not avoiding the interest. It is accounted for through the payoff and closing costs.”

Not as catchy, sure. But a lot more accurate.

What borrowers should focus on instead

Instead of asking, “Do I skip a payment?” the better questions are:

- What are my actual closing costs?

- How much prepaid interest is being collected?

- How long will it take me to recoup the cost of this refinance?

- Am I lowering my rate, changing my term, improving cash flow, or consolidating debt in a way that truly benefits me?

- Does this refinance make sense for my short-term and long-term goals?

That is the real conversation. Because a refinance should never be judged by a catchy phrase. It should be judged by math, timing, and whether it improves your financial position.

Bottom line

Do you skip a mortgage payment when you refinance? Not really.

You may experience a gap before your first new mortgage payment is due, but you are not getting a free month. Interest is still being paid. It is just being handled through the payoff of the old loan, prepaid interest on the new loan, and the way mortgage payments are scheduled.

The idea of “skipping a payment” sounds appealing, but it is more myth than money-saving strategy. When it comes to refinancing, the smartest move is not chasing a so-called skipped payment. It is understanding exactly where the money is going and whether the refinance truly serves your goals.

Feel free to reach out to me at 312-296-4175 or email me at connect@borislending.com. I’m here to help you navigate the process and make the right decisions. I lend in all 50 states and I am never too busy for your referrals!!

I have been in the mortgage industry since 1997 and I understand the anxiety that comes with making the most expensive investment of a lifetime. My objective is to be your advisor, to educate you and to make the mortgage loan transaction as transparent and as stress-free as possible. I enjoy establishing personal connections and work mostly by referral. I thoroughly explain the process and available options, and guide my clients to make choices that best fit their needs and financial goals. Once the underwriting begins I communicate regularly and keep my clients apprised of the loan status from the beginning through the end. My relationship with clients does not end at the closing table. You are my client for life and I am always available to answer your questions and provide you with guidance.