The 50-Year Mortgage: Does It Really Make Homes More Affordable?

A Clear Look at Amortization, Monthly Payments, and Long-Term Costs

The mortgage industry has been buzzing about the newly proposed 50-year mortgage. Supporters say it could help improve affordability in high-cost housing markets. Critics warn that it creates long-term financial risks for borrowers. Both sides agree on one thing: spreading payments over a longer period reduces the monthly payment.

But how much does it actually reduce the payment — and at what cost?

This is where many conversations have missed the mark. Most posts focus solely on the massive long-term interest burden, and that concern is absolutely valid. A 50-year mortgage dramatically increases total interest paid.

But here’s what hasn’t been explained clearly enough:

The monthly savings between a 30-year and a 50-year mortgage are surprisingly small — far smaller than consumers expect — because of how amortization works.

Below is a deeper look at why these savings shrink, how amortization actually distributes your payment, and what the real numbers look like on a standard $400,000 mortgage.

How Amortization Works (And Why It Matters)

Every traditional mortgage follows an amortization schedule. This means:

- Your payment stays the same every month (when the rate is fixed).

- The mix of principal and interest changes over time.

- At the beginning, the payment is mostly interest.

- Over time, more of each payment goes toward principal.

- The longer the term, the slower the principal gets paid down.

Now here’s the key insight:

The biggest reduction in monthly payment happens when you take the biggest jump in term length.

This is why going from a 15-year to a 30-year mortgage dramatically reduces the payment.

But once you’re already at a long term (30 years), stretching it further produces a much smaller benefit.

This is called diminishing returns of loan extension.

Let’s look at the numbers.

Payment Comparison: 15-Year vs 30-Year vs 50-Year Mortgages

Assuming a $400,000 loan amount

For realistic comparison, we’ll use approximate current rate spreads:

- 15-year fixed: lower rate

- 30-year fixed: standard rate

- 50-year fixed: often higher rate due to higher risk (I’ll include a 0.75% premium)

Assumed Rates for Illustration

- 15-Year Fixed: 5.50%

- 30-Year Fixed: 6.25%

- 50-Year Fixed: 7.00%

(Rates are for demonstration only—always check current pricing.)

Monthly Payment Breakdown (Principal & Interest Only)

15-Year Fixed — $400,000

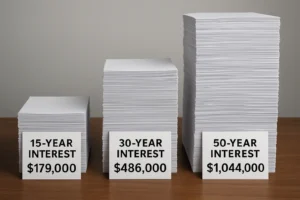

Payment: $3,268 / month

Total interest over 15 years: ~$178,878

30-Year Fixed — $400,000

Payment: $2,463 / month

Total interest over 30 years: ~$486,632

50-Year Fixed — $400,000

Payment: $2,407 / month

Total interest over 50 years: ~$1,044,052

The Real Takeaway: The Monthly Savings Are Tiny

Borrowers expect huge savings when stretching from 30 to 50 years. But look at the difference:

Difference Between 30-Year and 50-Year Payments

30-year: $2,462

50-year: $2,402

Savings: $56/month

Yes—just $56.

On a $500,000 loan, the savings are roughly $70/month.

Why the Payment Difference Is So Small

When you extend from 15 to 30 years, you’re doubling the term. That slashes the principal portion of the payment significantly.

But once you are already at 30 years, stretching even further yields very little benefit because:

- Interest dominates the early years of an amortized loan.

- The principal gets stretched so thin that reducing it even more doesn’t move the needle.

- The higher interest rate of a 50-year loan erases most of the potential savings.

In other words:

You’re giving the lender two extra decades for only a few dollars of monthly relief—and paying hundreds of thousands of dollars more over the life of the loan.

Comparing Lifetime Interest Paid

Here’s the part borrowers rarely see spelled out:

Total Interest Over the Life of the Loan

- 15-Year: ~$178,878

- 30-Year: ~$486,632

- 50-Year: ~$1,044,052

Going from 30 years to 50 years adds:

+ $557,400 in extra interest

All for about $56/month in savings.

That trade-off simply does not make financial sense for the overwhelming majority of borrowers.

A Smarter Alternative: A Simple Rate Buydown

Instead of a 50-year mortgage, a borrower can:

Buy down the rate on a 30-year fixed by 0.25%.

The cost of this buydown is usually a small fraction of what the borrower would lose in long-term interest.

A 0.25% rate reduction on a $400,000 30-year loan typically reduces the payment by:

~$64/month — the same savings as a 50-year mortgage, but without adding 20 more years of interest.

This is arguably:

- cheaper

- safer

- smarter

- easier to refinance

- better for long-term equity growth

The Real Risk: The “Affordability Illusion”

The 50-year mortgage looks like an affordability solution at first glance.

Smaller payment = easier qualification = more buyers in the market.

But the illusion falls apart fast when you realize that:

- the payment barely drops

- the long-term interest cost skyrockets

- equity builds painfully slowly

- borrowers become trapped if home values stagnate

- refinancing out later may be difficult if rates don’t drop significantly

This program risks creating borrowers who are house-poor today and financially restricted for decades.

The Bottom Line

The idea of a 50-year mortgage grabs attention because it sounds like a dramatic new solution to affordability challenges.

But the math tells a different story.

- The monthly savings compared to a 30-year loan are minimal.

- The long-term interest cost is massive.

- A simple 0.25% rate buydown provides similar monthly savings—without the financial damage.

This is why it will be critical for loan officers and real estate professionals to help clients understand not just the headline, but the underlying numbers. Consumers deserve clarity, not confusion. They deserve advice that protects their long-term financial well-being, not advice that sounds good in the moment but hurts them later.

Feel free to reach out to me at 312-296-4175 or email me at connect@borislending.com. I’m here to help you navigate the process and make the right decisions. I lend in all 50 states and I am never too busy for your referrals!!

I have been in the mortgage industry since 1997 and I understand the anxiety that comes with making the most expensive investment of a lifetime. My objective is to be your advisor, to educate you and to make the mortgage loan transaction as transparent and as stress-free as possible. I enjoy establishing personal connections and work mostly by referral. I thoroughly explain the process and available options, and guide my clients to make choices that best fit their needs and financial goals. Once the underwriting begins I communicate regularly and keep my clients apprised of the loan status from the beginning through the end. My relationship with clients does not end at the closing table. You are my client for life and I am always available to answer your questions and provide you with guidance.