You Didn’t Use Up Your VA Loan: How Entitlement Reuse Actually Works

One of the most valuable things a veteran owns is also one of the most misunderstood: the VA home loan benefit. I talk to veterans every week who assume that because they bought a home with a VA loan years ago, that door is closed. It isn’t. The benefit is yours for life, and in most cases you can use it again — sometimes without even selling the home you’re in now.

Let me clear up the two biggest misconceptions, because they cost people real money and real options.

Myth #1: “I already used my VA loan, so it’s gone.”

It’s not gone. The VA home loan benefit is a lifetime benefit, not a one-time card you punch once and hand back.

What actually gets used is something called your entitlement — the amount the VA guarantees to your lender on your behalf. When you close a VA loan, a portion of that entitlement gets tied up in the property. But “tied up” is not the same as “gone.” Once you sell that home and pay off the loan, the entitlement is restored, and you’re right back to where you started. Plenty of the veterans I finance are on their second, third, or fourth VA loan.

Here’s what that means in plain terms: buying one home with a VA loan does not disqualify you from buying another one with a VA loan. Your Certificate of Eligibility shows exactly how much entitlement you’ve used and how much you have left. If you don’t know your number, that’s the first thing worth finding out.

Myth #2: “I have to sell my current home before I can use it again.”

This is the one that surprises people most. You may be able to buy a second home with a VA loan while keeping the first one — and even rent it out.

The mechanism is called second-tier entitlement (sometimes called bonus entitlement). If you have entitlement left over after your first loan, you can put it toward a second VA loan without paying off the first. This comes up constantly with military families who get PCS orders, don’t want to sell in a soft market, and turn the old house into a rental instead of a fire sale.

The occupancy rule still applies — VA loans are for a home you intend to live in, not an investment property. But if you genuinely occupied that first home as your primary residence, converting it to a rental after you move is perfectly allowed. You satisfied the requirement when you lived there.

How the second-time math actually works

This is where it helps to see the numbers, so here’s a clean example.

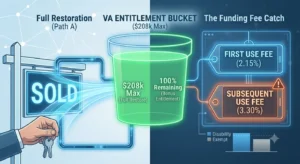

The VA guarantees 25% of your loan, and lenders generally want that full 25% covered before they’ll do zero down. In a county with the 2026 baseline loan limit of $832,750, the most entitlement available works out to about $208,000 (25% of that limit).

Say your first VA loan was on a $300,000 home. That used roughly $75,000 of entitlement (25% of $300,000). Subtract that from your $208,000, and you’ve got about $133,000 of entitlement left. Because lenders want 25% coverage, that remaining entitlement supports a second zero-down loan of roughly $533,000 — while your first home stays put, ideally paying you rent.

Two things to keep in mind. First, if the second home costs more than your remaining entitlement covers, you’re not shut out — you’d just put down 25% of the difference, not 25% of the whole price. Second, if you have your full entitlement available, there is no VA loan limit at all; your loan amount is capped only by what you actually qualify for. These numbers move with your county’s limit and your exact entitlement, so treat the example as the shape of it, not your answer. Running your real figures is a ten-minute conversation.

Restoring your entitlement — and the one detail people miss

There are two ways to get your entitlement back for full reuse.

The standard path: sell the home and pay off the VA loan. Once the loan is satisfied and the property is out of your name, you apply to restore your entitlement and you’re back to full.

The lesser-known path: a one-time restoration. If you paid off your VA loan but kept the home — say you refinanced it into a conventional loan — you can restore your entitlement one time without selling. It’s a single use, so it’s worth spending on purpose.

Here’s the detail almost nobody mentions: restoring your entitlement makes it available again, but it does not reset your funding fee to the first-use rate. Once you’ve used a VA loan, you’re a subsequent user for funding fee purposes, restoration or not. Knowing that up front keeps the closing costs from surprising you.

What it costs the second time

The VA funding fee is higher on repeat use. For 2026, a first-time buyer with no money down pays 2.15%; a subsequent user with no money down pays 3.30%. On a $400,000 loan, that’s the difference between about $8,600 and $13,200 — not nothing.

But you have levers. Put 5% down and the subsequent-use fee drops to 1.50%, wiping out most of the repeat-use penalty. And if you receive VA disability compensation at any rating, you’re exempt from the funding fee entirely — first use or fifth. A surprising number of eligible veterans pay a fee they never owed, so check your Certificate of Eligibility before you sign anything.

The bottom line

Your VA benefit didn’t expire the day you closed your first loan. Between second-tier entitlement, restoration, and the option to keep your current home as a rental, you have more room to move than most people realize — and a few decisions, like when to make a down payment or restore entitlement, are worth making deliberately rather than by default.

Before you assume you’re out of options, or that reusing your benefit is automatically the right move, let’s look at your actual entitlement and run the numbers. Sometimes the answer is “yes, and here’s how.” Sometimes it’s “wait.” Either way, you’ll know exactly where you stand.

Feel free to reach out to me at 312-296-4175 or email me at connect@borislending.com. I’m here to help you navigate the process and make the right decisions. I lend in all 50 states and I am never too busy for your referrals!!

I have been in the mortgage industry since 1997 and I understand the anxiety that comes with making the most expensive investment of a lifetime. My objective is to be your advisor, to educate you and to make the mortgage loan transaction as transparent and as stress-free as possible. I enjoy establishing personal connections and work mostly by referral. I thoroughly explain the process and available options, and guide my clients to make choices that best fit their needs and financial goals. Once the underwriting begins I communicate regularly and keep my clients apprised of the loan status from the beginning through the end. My relationship with clients does not end at the closing table. You are my client for life and I am always available to answer your questions and provide you with guidance.