7 (Plus a Few More) Financial Instruments Every Household Should Have

Owning a home is one of the greatest milestones in personal finance. It represents stability, pride, and often, the largest asset in your family’s portfolio. But let’s be honest: a house is also a financial responsibility with layers of hidden costs, risks, and “what ifs” that can surprise even seasoned homeowners.

That’s where financial instruments come in. Think of them as the protective gear every homeowner should wear — not glamorous, but essential if you want to stay safe while building wealth. Without them, even a small stumble can turn into a financial fall.

In this guide, I’ll explore seven essential financial tools that every household should have, plus a few bonus ones that smart homeowners keep in their back pocket. For each, you’ll see not only why they matter, but also how they connect to the realities of homeownership — whether you’re making your very first mortgage payment or you’ve been in your home for decades.

1. A Working Home Budget

Let’s start with the unglamorous, unsung hero of financial success: the budget. A home budget isn’t just a list of numbers. It’s a map of your financial life, showing you where your money comes from, where it goes, and what’s left to build security.

Why it matters for homeowners:

- Tracks real costs of ownership: Mortgage payments are only the beginning. Add in property taxes, homeowners insurance, utilities, HOA fees, lawn care, and inevitable repairs, and suddenly the “affordable” home stretches the budget. A working budget shines a light on these recurring costs.

- Prevents overextension: Owning a home often tempts families to upgrade furniture, buy new cars, or start ambitious projects. A budget keeps spending anchored in reality, preventing “lifestyle creep.”

- Safeguards mortgage payments: Falling behind on your mortgage can be financially devastating. A budget prioritizes essential bills so the roof over your head stays protected.

For new homeowners: Budgets are critical in the first year, when you’re still learning what “normal” costs look like. That first water bill, for example, is rarely what you expected.

For long-time owners: A budget helps you plan for bigger-ticket items like renovations, paying down principal faster, or even upgrading to your next home.

In short, a budget is the flashlight that keeps you from tripping over the unseen costs of ownership.

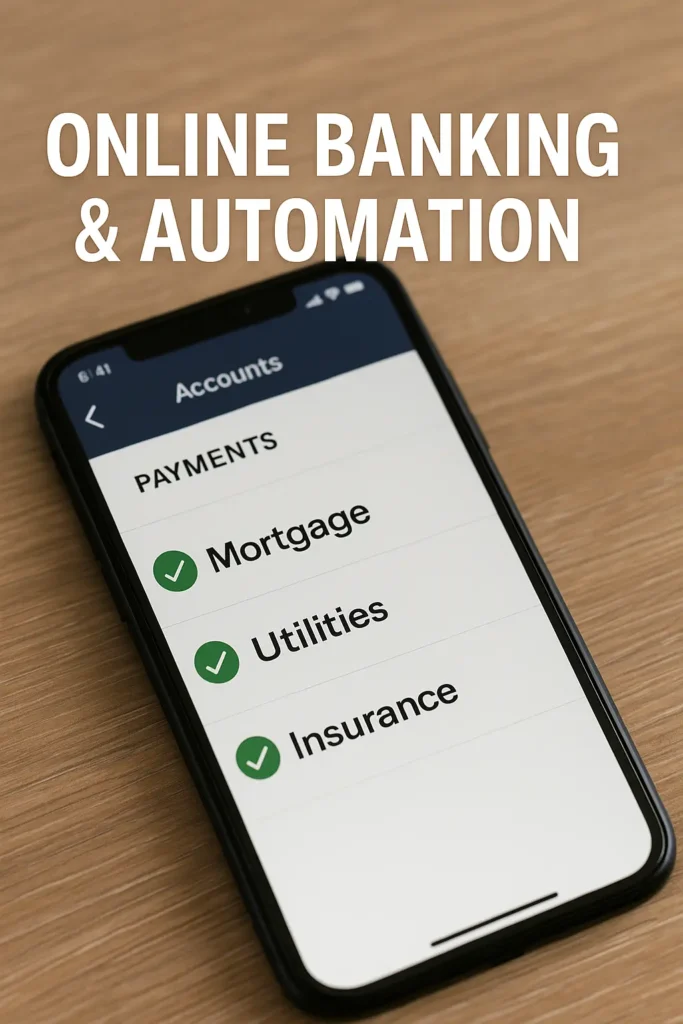

2. Online Banking to Organize Bill Payments

We live in a digital world. Yet too many households still rely on memory, sticky notes, or outdated calendars to pay bills. Online banking is the modern tool that keeps you on track, and when it comes to homeownership, missing even a single payment can have serious consequences.

Why it matters for homeowners:

- Prevents late fees and credit dings: Mortgage payments reported late can devastate a credit score. Online banking lets you automate payments to avoid slip-ups.

- Centralizes cash flow: Linking mortgage, utilities, and insurance bills to your online banking gives you a clear picture of what’s due and when.

- Supports savings goals: Most platforms allow sub-accounts or tracking categories, helping you earmark money for home improvements, taxes, or emergency reserves.

Think of it this way: you don’t manually crank down your garage door anymore — why should you manually manage every recurring bill? Automation is financial peace of mind.

3. A Significantly Sized Life Insurance Policy

Homeownership is about providing stability. But what happens if the primary income earner suddenly isn’t there to provide? That’s where life insurance steps in. It’s not about money — it’s about keeping your family in their home during life’s hardest moments.

Why it matters for homeowners:

- Mortgage protection: A well-sized policy ensures your spouse or children can continue paying the mortgage — or even pay it off in full.

- Maintains continuity: It prevents the trauma of losing a loved one from being compounded by losing the family home.

- Covers broader costs: Insurance proceeds can also fund property taxes, maintenance, and daily living expenses.

How much is “significantly sized”? A good rule is coverage that at least equals your mortgage balance plus five to ten years of household expenses. This isn’t about leaving behind luxury — it’s about leaving behind security.

4. A Will

Few topics get procrastinated more than writing a will. But if you’re a homeowner, this isn’t optional — it’s a responsibility. Without a will, your state decides who inherits your assets. That can mean delays, legal costs, and family disputes.

Why it matters for homeowners:

- Clarifies ownership: Your home is likely your largest asset. A will makes clear who receives it and under what conditions.

- Reduces costs and delays: Probate without a will can tie up assets for months, leaving your family financially vulnerable.

- Protects dependents: Parents can name guardians for children and outline how assets are managed until they’re adults.

Writing a will is the financial equivalent of changing the locks on your home — it keeps things safe and under your control.

5. Automatic Withdrawals Into Savings

If savings depends on “leftover money,” it rarely happens. Automatic transfers are the secret to building reserves without relying on willpower.

Why it matters for homeowners:

- Funds repairs and upgrades: Even the best-maintained home eventually needs a roof, HVAC system, or remodel. Automated savings creates a home maintenance fund.

- Builds future opportunity: It positions you for bigger goals like an investment property or early mortgage payoff.

- Builds discipline by design: If money moves to savings before you see it, you’re less tempted to spend it.

For homeowners, automatic savings is like setting your thermostat — you don’t have to think about it every day, but it keeps the environment comfortable.

6. Three to Six Months’ Reserves in Cash

This one can’t be overstated. An emergency fund isn’t a luxury — it’s a necessity.

Why it matters for homeowners:

- Keeps the mortgage paid: If income is interrupted due to job loss or illness, reserves protect your standing with the lender.

- Covers sudden expenses: From a broken water heater to a leaky roof, emergencies never wait until your bank account is ready.

- Reduces reliance on debt: Having cash means you won’t need high-interest credit cards or risky loans to handle surprises.

Aim for three to six months of essential expenses, stored in a high-yield savings account that’s easy to access in an emergency but not so easy that you dip into it for non-essentials. It’s the difference between a stressful situation and a financial crisis.

7. Health and Disability Insurance

Many households underestimate the role of insurance in protecting homeownership. But the truth is simple: you can’t keep your home if you lose your ability to earn.

Why it matters for homeowners:

- Health insurance: Prevents medical bills from draining savings or forcing tough choices between care and mortgage.

- Disability insurance: Provides income replacement if you’re unable to work due to illness or injury.

- Protects long-term plans: Especially critical in single-income households, where losing one paycheck can derail everything.

It’s hard to imagine, but medical issues are one of the leading causes of foreclosure. Protecting your health is also protecting your home.

Other Financial Instruments Worth Considering

- Homeowners Insurance Review: Make sure your coverage reflects current rebuilding costs, personal property, and any improvements you’ve made.

- Umbrella Liability Policy: Adds a layer of liability protection in case of accidents on your property that exceed standard policy limits.

- Living Trusts and Powers of Attorney: Going beyond a will, these documents give clearer instructions and help avoid probate altogether.

- Retirement Accounts (401k/IRA): While not tied directly to the mortgage, retirement planning ensures you won’t be house-rich but cash-poor later in life.

- Credit Monitoring and Identity Theft Protection: With so much of your financial life tied to your mortgage and credit profile, proactive monitoring is wise.

Bringing It All Together

Homeownership isn’t just about making monthly payments — it’s about building a foundation of financial security. Each of these instruments plays a specific role:

- A budget keeps spending aligned.

- Online banking prevents mistakes.

- Life insurance protects your family.

- A will protects your legacy.

- Automatic savings builds reserves.

- Emergency cash prevents crises.

- Insurance coverage shields your income and health.

Together, they form a safety net that keeps your home — and your financial life — secure, no matter what life throws your way.

Final Thoughts

Whether you’re a brand-new homeowner adjusting to your first mortgage or a seasoned one planning the next stage of life, the right financial instruments make all the difference. They turn uncertainty into preparedness and transform your home from just a place you live into a cornerstone of long-term wealth.

The key is not to tackle everything at once. Start with the basics: a budget, automated savings, and a modest emergency fund. Then layer in protections like insurance and estate planning. Over time, you’ll build a comprehensive system that makes your financial life more resilient.

If you’d like help understanding how these financial instruments fit into your personal homeownership strategy, let’s connect. As your mortgage advisor, my role isn’t just helping you secure the loan — it’s helping you succeed as a homeowner long after closing day. Feel free to reach out to me at 312-296-4175 or email me at connect@borislending.com. I lend in all 50 states and I am never too busy for your referrals!!

I have been in the mortgage industry since 1997 and I understand the anxiety that comes with making the most expensive investment of a lifetime. My objective is to be your advisor, to educate you and to make the mortgage loan transaction as transparent and as stress-free as possible. I enjoy establishing personal connections and work mostly by referral. I thoroughly explain the process and available options, and guide my clients to make choices that best fit their needs and financial goals. Once the underwriting begins I communicate regularly and keep my clients apprised of the loan status from the beginning through the end. My relationship with clients does not end at the closing table. You are my client for life and I am always available to answer your questions and provide you with guidance.